Instant stablecoin top-up methods compared

Choosing how to fund your wallet is the first step in acquiring stablecoins. The method you select dictates your speed, your costs, and your security posture. There is no single best option; the right choice depends on whether you prioritize immediate access or lower fees.

Credit and debit cards offer the fastest route to on-chain liquidity. Your funds usually appear in minutes, but exchanges charge a premium for this convenience. Bank transfers and peer-to-peer (P2P) markets are significantly cheaper but require more time and diligence. Understanding these trade-offs helps you avoid unnecessary friction when moving capital.

The table below outlines the standard performance metrics for each funding method. Use this to gauge which approach fits your immediate needs, keeping in mind that fees and speeds can vary by platform and region.

| Method | Speed | Fee % | Risk Level |

|---|---|---|---|

| Credit Card | Instant | 3-5% | High (chargebacks) |

| Debit Card | Instant | 1-3% | Medium |

| Bank Transfer (SEPA/ACH) | 1-3 Days | 0-1% | Low |

| P2P Markets | Minutes | 0-1% | Medium (escrow needed) |

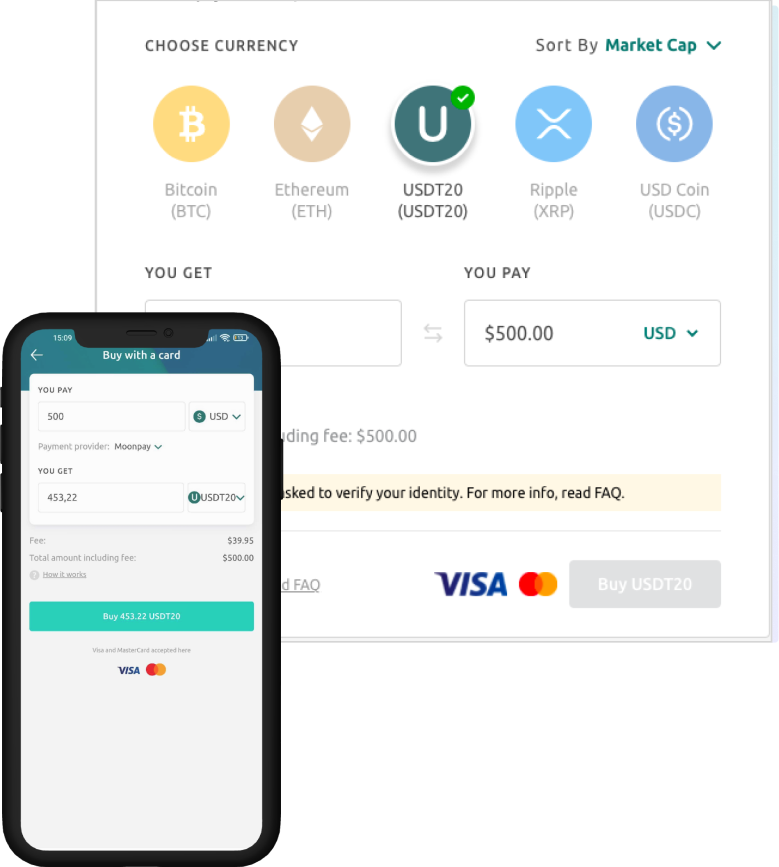

Credit cards are the most convenient but also the most expensive way to buy crypto. Because these transactions are treated as cash advances by many issuers, you may face additional interest charges and higher fraud risk. Debit cards are slightly cheaper but still carry the same instant-settlement premium.

Bank transfers, such as SEPA in Europe or ACH in the US, are the most cost-effective for larger sums. However, they are not instant. Settlement can take one to three business days, which is a significant delay if you need to capitalize on a market move immediately.

Peer-to-peer (P2P) markets offer a middle ground. You can buy directly from other users at near-market rates with low fees. The trade-off is that you must manage the escrow process yourself or rely on the platform's escrow service, which requires careful verification to avoid scams.

As an Amazon Associate, we may earn from qualifying purchases.

Credit card top-up fees and cash advance risks

Using a credit card for stablecoin purchases often looks convenient at first glance, but the hidden costs can severely erode your capital. Unlike a standard purchase, crypto transactions are frequently classified by card issuers as "cash advances." This reclassification triggers immediate financial penalties that apply before you even hold the stablecoins.

The primary danger lies in the interest rate. When a transaction is flagged as a cash advance, the standard purchase APR is replaced by a much higher cash advance APR. More importantly, interest begins accruing immediately from the moment the transaction clears. There is no grace period, meaning you owe interest on day one, regardless of when you pay your bill. This can turn a simple deposit into a high-interest debt trap if the stablecoin's value does not appreciate enough to offset the cost.

In addition to the interest rate hike, most issuers charge a flat cash advance fee, typically ranging from 3% to 5% of the transaction amount, with a minimum charge. These fees are added directly to your balance. When you combine the upfront fee with the immediate, high-interest accrual, the effective cost of acquiring stablecoins via credit card can exceed 10% or more in just the first month.

To avoid these penalties, it is essential to review your cardholder agreement before initiating any crypto-related deposit. Look specifically for sections detailing "cash equivalents" or "quasi-cash transactions." If your issuer lists cryptocurrency purchases as cash advances, the method is likely too expensive for regular use. Consider bank transfers or debit card options instead, which typically avoid these punitive fee structures.

Bank transfers for low-fee stablecoin deposits

Bank transfers remain the most cost-effective method for stablecoin deposits, primarily because they bypass the high processing fees associated with credit cards. When you use ACH (Automated Clearing House) or wire transfers to buy USDT or USDC, you are moving fiat currency directly through traditional banking rails. This direct path eliminates the intermediary fees that credit card processors charge to mitigate fraud risk.

The primary trade-off is time. While credit card purchases settle in minutes, ACH transfers typically take one to three business days to clear. Wire transfers are faster, often arriving within hours, but they come with their own set of bank-imposed fees that vary by institution. For investors who prioritize capital preservation over instant access, this delay is a manageable friction point.

ACH vs. Wire: Speed and Cost

| Feature | ACH Transfer | Wire Transfer |

|---|---|---|

| Typical Fee | $0 - $5 per transaction | $15 - $30 per transaction |

| Settlement Time | 1-3 Business Days | Same Day or Next Day |

| Best For | Large, non-urgent deposits | Urgent, high-value deposits |

Security and Transparency

Using bank transfers for stablecoin deposits offers a layer of security that credit cards cannot match. Credit cards are chargeback-prone, meaning exchanges may freeze your account if a dispute arises. Bank transfers are final; once the funds leave your account, the transaction is irreversible. This reduces the risk of your funds being held in limbo due to payment disputes.

As noted by industry analysts in 2026, stablecoins are increasingly viewed as a predictable rail for businesses needing transparency (Thunes, 2026). Bank transfers align with this trend by providing a clear, auditable trail from your bank to the exchange. This transparency is crucial for high-stakes finance, where fee clarity and security are paramount.

When to Use Bank Transfers

Bank transfers are ideal for long-term holders who do not need immediate liquidity. If you are accumulating USDC for yield farming or holding USDT for cross-border payments, the one-to-three-day wait is negligible compared to the 3-5% fee savings from avoiding credit card transactions. For smaller amounts, the fixed wire fees may make ACH the only viable low-cost option.

Key Takeaways

- Lower Fees: ACH and wire transfers cost significantly less than credit card purchases.

- Slower Settlement: Expect 1-3 days for ACH; wires are faster but more expensive.

- Finality: Bank transfers are irreversible, reducing dispute-related freezes.

- Best For: Large, non-urgent deposits where fee savings outweigh speed.

Choosing the right stablecoin top-up method for your needs

The best approach depends on whether you prioritize speed or cost. Credit card purchases offer immediate liquidity but come with high processing fees, while bank transfers provide lower costs but require patience for settlement.

If you need funds instantly for a trade or payment, credit cards are the standard choice. Most major exchanges process these deposits within minutes. However, expect fees ranging from 3% to 5%, which can erode small profits. This method is best for emergency liquidity or time-sensitive opportunities.

For larger amounts or non-urgent transfers, bank wires and ACH transfers are significantly cheaper. ACH deposits typically cost nothing or a flat fee under $10, but they take 1-3 business days to clear. Use this route when you are funding your wallet for long-term holding rather than immediate speculation.

Before committing, check your exchange’s daily limits and security requirements. Credit cards may trigger fraud alerts for large crypto purchases. Ensure your bank allows international transfers if you are using a non-domestic exchange. Always start with a small test deposit to confirm the flow works as expected.

Use this checklist to finalize your decision:

-

Confirm the deposit fee percentage for your chosen method.

-

Verify that your bank or card issuer allows crypto transactions.

-

Check your exchange’s daily deposit limits for the selected payment type.

-

Ensure your wallet address matches the supported network (e.g., ERC-20, TRC-20).

Match your method to your timeline. If speed is critical, pay the premium for credit cards. If cost efficiency matters more, wait for the bank transfer to clear.

Top stablecoins for 2026 top-ups

When funding your wallet, liquidity is your primary safety net. A stablecoin top-up strategy relies on assets that are instantly convertible and widely accepted across exchanges. The market is dominated by two giants: Tether (USDT) and USD Coin (USDC). These two assets account for over 85% of the stablecoin supply on Ethereum mainnet, ensuring that your funds are never stranded due to lack of buyers or sellers.

Tether (USDT) remains the largest stablecoin by circulating supply, holding approximately $58 billion in value as of April 2026 [1]. Its massive adoption makes it the default choice for high-volume traders and cross-border payments where speed and universal acceptance matter most. However, its sheer size also means regulatory scrutiny is intense.

USD Coin (USDC) sits in second place with roughly $38 billion in circulating supply [1]. Backed by regulated financial institutions, USDC is often preferred for its transparency and compliance with US regulations. For a stablecoin top-up, choosing between USDT and USDC usually comes down to which exchange you use; both offer the same dollar stability, but one may have lower fees or faster settlement times depending on your platform.

1

Frequently asked questions about stablecoin top-ups

What is the top stablecoin in 2026?

Tether (USDT) remains the largest stablecoin by circulating supply, holding approximately $58 billion on Ethereum mainnet as of April 2026. USDC follows in second place with roughly $38 billion. Together, these two assets account for over 85% of the stablecoin supply on Ethereum, making them the most liquid options for stablecoin top-ups. Other notable contenders like DAI and USDe sit in the $3–6 billion range each.

Which stablecoins are safest for top-ups?

Safety in stablecoins comes from regulatory compliance and reserve transparency. USDC is widely regarded as a safer choice for institutional and high-value transfers because it adheres to strict US regulatory standards and publishes regular attestation reports. USDT is also safe for general use but operates under different regulatory frameworks. For stablecoin top-ups, prioritize assets that are fully backed by cash and short-term government treasuries to minimize de-pegging risks.

How do I choose the right stablecoin for my needs?

Selecting a stablecoin depends on your primary goal: speed, cost, or regulatory safety. USDT offers the deepest liquidity across most exchanges, ensuring faster execution. USDC provides greater transparency and is preferred by US-based financial institutions. If you are operating in Europe, EURC may be relevant for Euro-denominated transactions. Always verify the network compatibility (e.g., ERC-20, TRC-20) to avoid losing funds during the top-up process.

No comments yet. Be the first to share your thoughts!