How stable card funding works in 2026

Stablecoin-linked payment cards bridge the gap between digital assets and everyday commerce, but the mechanics behind the plastic vary significantly by provider. To understand how these cards load funds, you need to distinguish between two distinct financial layers: the on-chain stablecoin balance held in your crypto wallet and the fiat-loaded balance sitting on the prepaid card itself.

Most programs operate on a pre-funded or prepaid model. This means your on-chain holdings—whether USDC, USDT, or USDP—do not automatically spend when you swipe the card. Instead, you must manually sell your stablecoins within the app to convert them into fiat currency, which then loads onto the card’s balance. Only after this conversion can you spend at merchants that accept traditional Visa or Mastercard networks.

This separation is intentional. It allows issuers to comply with traditional banking regulations while still offering the speed of digital asset management. When you load funds, you are essentially moving value from a blockchain ledger to a centralized banking ledger. Understanding this flow is critical because it dictates the speed, fees, and security protocols you will encounter with every funding method we discuss below.

Top instant reload methods compared

Choosing the right funding method depends on balancing speed against cost. While all three primary channels—bank transfers, crypto swaps, and direct deposits—fund your balance, they operate on different timelines and fee structures. Understanding these mechanics helps you avoid unnecessary friction when spending.

Bank transfers and direct deposits

Traditional bank transfers (ACH) and direct deposits remain the most common way to fund stable cards. These methods are generally free but slow. A standard ACH transfer can take one to three business days to clear, meaning your spending power is delayed. Direct deposits from employers are also free and often qualify for faster availability under Regulation CC, but they are tied to your pay cycle rather than your immediate liquidity needs. For users who prefer low fees over instant access, this is the standard approach.

Crypto swaps and stablecoin conversions

For users holding crypto assets, swapping tokens into a stablecoin balance offers instant access. Most stable card apps include an integrated swap feature that converts assets like ETH or BTC into USDC or USDT in seconds. While the speed is unmatched, the cost varies. You may face network gas fees, exchange spreads, or platform-specific swap fees. This method is ideal for users who need immediate liquidity but are willing to pay a premium for speed. Always check the current network congestion before executing a swap to avoid high gas costs.

Comparison of funding channels

The table below outlines the typical trade-offs between these methods. Note that specific limits and fees depend on the individual card issuer and your verification tier.

| Method | Speed | Typical Cost | Typical Limit |

|---|---|---|---|

| Bank Transfer (ACH) | 1-3 business days | Free | Up to $20,000 |

| Direct Deposit | Same-day (varies) | Free | Varies by issuer |

| Crypto Swap | Instant | Network/Platform fees | Wallet balance |

Choosing the right balance

Most users benefit from a hybrid approach. Use direct deposits for steady, fee-free funding of your base spending needs. Keep a small crypto reserve for instant reloads when unexpected expenses arise. This strategy minimizes fees while ensuring you always have available funds. Always verify the specific limits of your card, as some providers cap monthly loads regardless of the funding source.

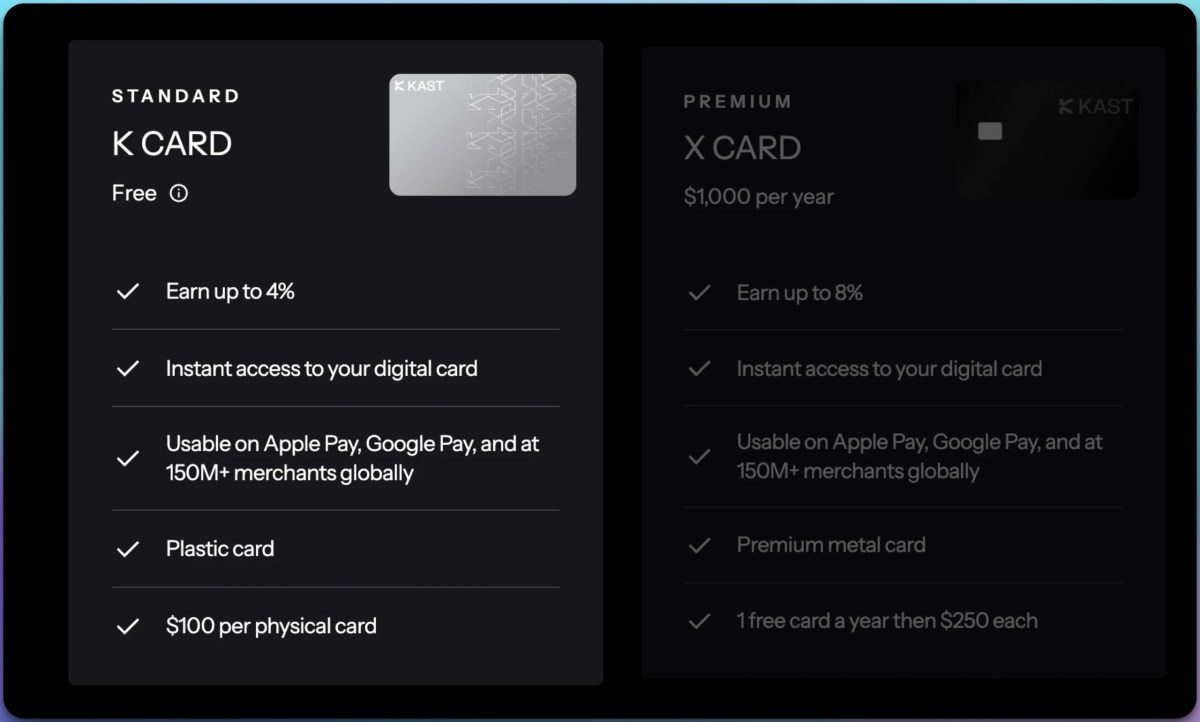

Best stablecoin card options for 2026

Choosing the right prepaid card depends on how you plan to load funds and where you spend them. For users seeking a reliable link between digital assets and daily purchases, the STABLE Visa Card remains a primary contender. It allows you to load funds directly from your STABLE Account, supporting flexible reloads up to $20,000 at a time. Because it operates on the Visa network, you can use it anywhere Visa is accepted, making it a practical bridge for stablecoin holders who need to spend in the real world without converting to fiat in a separate step.

When selecting a stablecoin-linked card, prioritize providers that offer transparent fee structures and robust security features. Look for cards that support instant loading via bank transfer or crypto wallet integration, as this reduces the friction of moving funds from your digital storage to your physical wallet. Security features like virtual card numbers and real-time transaction alerts are essential for protecting your assets against fraud.

For those who prefer a more traditional approach or need a backup option, consider exploring other major prepaid card providers that support crypto-friendly funding sources. Many of these cards are available through major retailers and often come with useful accessories like secure card holders. The following selection highlights some of the most highly regarded options for managing your stablecoin spending in 2026.

As an Amazon Associate, we may earn from qualifying purchases.

Understanding fees and hidden costs

When you choose a stable card funding method, the headline rate is rarely the final price. Banks and prepaid card issuers layer charges that only appear on your monthly statement or after a specific action. For a stable card, these costs directly erode the stable value you are trying to preserve. You need to know exactly what triggers a fee before you load funds.

Monthly maintenance and inactivity

Many prepaid cards, including the STABLE Visa Card, charge a monthly service fee if the account balance falls below a certain threshold or if you do not use the card for a set period. These fees are often small, around $2 to $5, but they compound over time. If you are holding a stable card as a savings vehicle rather than a daily spending tool, an inactivity fee can silently drain your principal. Always check the cardholder agreement for "dormancy" clauses that define how long you can go without a transaction before penalties apply.

ATM withdrawal and cash advance fees

The most expensive surprise for stable card users is the ATM fee. Unlike traditional bank accounts, stable cards often treat cash withdrawals as cash advances or incur a flat fee per transaction. If you withdraw $50 from an out-of-network ATM, you might pay a $3 card fee plus a $2 network surcharge. Worse, some cards apply interest immediately on the withdrawn amount. If you need cash, use in-network ATMs whenever possible and withdraw larger amounts less frequently to minimize the number of transactions.

Cross-border and currency conversion

If you travel or buy from international merchants, your stable card may apply a foreign transaction fee. This is typically a percentage of the purchase amount, ranging from 1% to 3%. Since stablecoins are pegged to the US dollar, you are effectively converting USD to another currency and back. Some cards waive this fee for specific tiers or if you use their proprietary exchange rate. Compare this against the spread offered by your funding method; sometimes paying a small reload fee is cheaper than paying a 3% foreign transaction fee later.

Secure your stable card funding

Funding your card is the moment most vulnerable to error. A single slip—like entering details on a fake portal—can drain the balance before you notice. Treat every reload like a bank transfer: verify the destination, protect the credentials, and watch the ledger.

Turn on 2FA immediately. Use an authenticator app or hardware key instead of SMS. If your card provider supports it, enable biometric login for the funding app. This blocks access even if your password leaks.

Always type the provider’s address manually or use a saved bookmark. Do not click links from emails or social media. Check for https:// and the correct domain name. Phishing sites often mimic real portals with one-letter changes.

Set up instant push notifications for every transaction. Review your card’s transaction history weekly. If you see a charge you didn’t make, freeze the card immediately through the app. Most providers allow instant card locking.

Keep your device secure. Use a strong, unique password for your card account. Avoid public Wi-Fi when funding. If you must use it, connect through a trusted VPN. These steps protect your stable card funding from common threats.

Frequently asked questions about stable card funding

How much can I add to my STABLE Card? You can load as much or as little as you need, anytime, up to a lifetime limit of $20,000. This cap applies to the standard annual contribution limit for ABLE accounts.

Can I contribute more if I am working? Yes. Over and above the standard $20,000 annual limit, a working beneficiary is allowed to contribute an additional amount up to the federal poverty line or their earned income, whichever is lower. This allows for larger reloads if you have a steady income source.

How long does a funding method take to process? Most electronic transfers from a linked bank account or debit card are processed instantly, allowing you to spend the funds immediately. If you are using a wire transfer or ACH batch, it may take one to three business days to clear.

Are there fees for loading my card? STABLE does not charge fees for adding money to your card. However, if you are using a third-party bank to send funds, that institution may apply standard transfer fees depending on your account type.

No comments yet. Be the first to share your thoughts!