Stable card up 2026 budget

The STABLE account landscape for 2026 centers on the ABLE Age Adjustment Act, which fundamentally shifts how much you can contribute annually. The standard federal limit remains $20,000 per year, but the new ABLE to Work Act allows eligible working individuals to contribute an additional $15,650 from their earned income. This brings the potential annual contribution ceiling to $35,650, offering a significant boost for those balancing employment with disability-related expenses.

When evaluating STABLE accounts, the tradeoff lies in account fees versus investment returns. Most providers charge annual maintenance fees ranging from $20 to $100, which can eat into your balance if not offset by strong investment performance. Look for accounts that offer low-cost index fund options or cash management alternatives with competitive interest rates. Since STABLE accounts are tax-advantaged, every dollar saved from Medicaid and SSI asset limits is worth more than a standard savings account.

For those looking to maximize their 2026 contributions, consider pairing your STABLE account with other tax-advantaged vehicles. High-yield savings accounts or short-term Treasury ETFs can serve as temporary holding tanks for funds before they are invested within your STABLE account. This strategy helps ensure your money is working for you immediately, rather than sitting idle while waiting for the next contribution cycle.

Shortlist real options

Loading your stable card in 2026 usually means choosing between speed, cost, and convenience. While some providers offer instant top-ups, others require manual conversion of crypto assets into fiat before spending. Understanding these tradeoffs helps you avoid unexpected fees or declined transactions.

The STABLE Visa Card offers a straightforward prepaid model. You can load any amount up to the annual limit of $20,000 directly from your linked bank account. This method is reliable for users who prefer fiat transfers over crypto conversions. For those holding digital assets, the pre-funded model requires you to manually sell stablecoins within the app before spending, which adds a step but keeps transaction costs predictable.

Comparison of Top-Up Methods

| Method | Speed | Best For | Primary Limit |

|---|---|---|---|

| Bank Transfer (ACH) | 1-3 days | Budgeting, low fees | $20,000/year |

| Instant Card Load | Seconds | Immediate spending | Varies by provider |

| Crypto Conversion | Minutes | Crypto holders | Network limits |

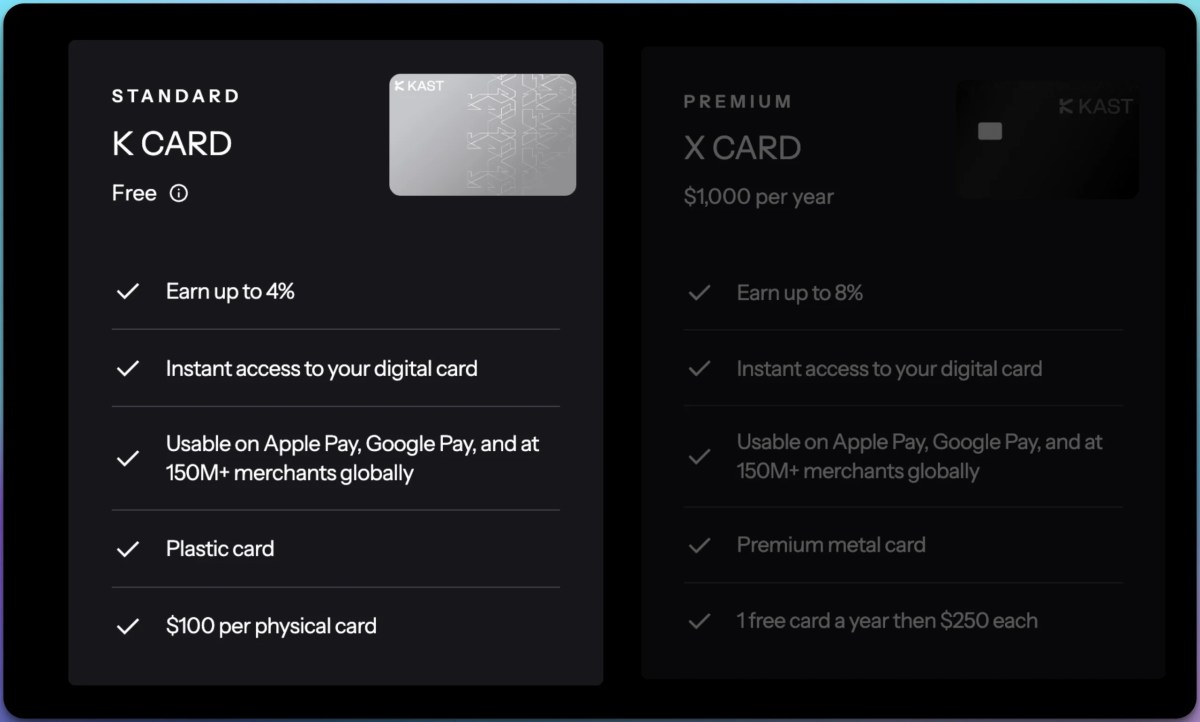

Top Picks for 2026

For users seeking a reliable prepaid card with flexible loading options, consider these popular choices available on Amazon:

As an Amazon Associate, we may earn from qualifying purchases.

What to Watch For

Always check the annual contribution limits. Under the ABLE to Work Act, eligible individuals can contribute up to an extra $15,650 in 2026 if they are working, in addition to the standard $20,000 limit. For general users, stick to official providers to ensure your funds are secure and your top-ups are processed instantly.

Inspect the expensive parts

Before you commit to a topping-up method, check for the fees that silently eat your balance. A $2 reload fee on a $50 top-up is a 4% loss, which no interest rate can recover. We break down the specific failure points to watch for so your money stays in your account, not in processing fees.

Many prepaid and stablecoin cards charge a flat fee for every instant transfer from a bank or crypto wallet. Look for "instant transfer" or "reload" fees in the fee schedule. If the fee is higher than 1-2%, switch to a zero-fee provider or use ACH transfers, which take 1-3 days but cost nothing.

If you are topping up with crypto, check the network gas fees. Ethereum mainnet can cost more than the top-up amount during busy periods. Stick to low-fee networks like Solana or Polygon for stablecoin transfers. Also, confirm if the card issuer charges a currency conversion fee if your funding source is in a different currency than your card balance.

Some cards charge a monthly fee if the balance drops below a certain threshold or if you don't make a purchase. Ensure your top-up strategy keeps you above the minimum balance to avoid these automatic deductions. Check if the card offers fee waivers for direct deposits or minimum spending volumes.

As an Amazon Associate, we may earn from qualifying purchases.

Ownership Costs and Hidden Fees

A low purchase price rarely tells the whole story. When you buy a debit card, you are entering a contract with ongoing fees that can erode your balance faster than you expect. The cheapest card upfront often carries the highest monthly maintenance charges or ATM withdrawal fees.

Before committing, check for these common costs:

- Monthly maintenance fees: Some cards charge $5–$10 monthly unless you meet specific spending thresholds.

- ATM withdrawal fees: Look for cards that reimburse ATM fees or have zero-fee networks.

- Inactivity fees: Some providers charge if you don’t use the card for 3–6 months.

- Reload fees: Adding money to your card can sometimes cost a percentage of the deposit.

Choosing the Right Card

Use the tools below to compare features and find a card that fits your budget.

As an Amazon Associate, we may earn from qualifying purchases.

Where to Put Your Money in 2026

If you are looking for better returns on your cash, consider these options:

No comments yet. Be the first to share your thoughts!