Stable card up 2026 budget

Top Up Your Stable Card Instantly requires verifying the source, comparing the total cost, and confirming post-payment support before you commit. Write down the one risk that would change your mind—such as uncertain seller conditions, hidden fees, or slow shipping—and resolve it before moving to checkout.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Inspect the expensive parts

Define the constraint, compare realistic options, and choose the path with the fewest hidden costs. This sequence keeps the advice usable by forcing a check on whether the recommendation fits your actual situation, budget, and timing.

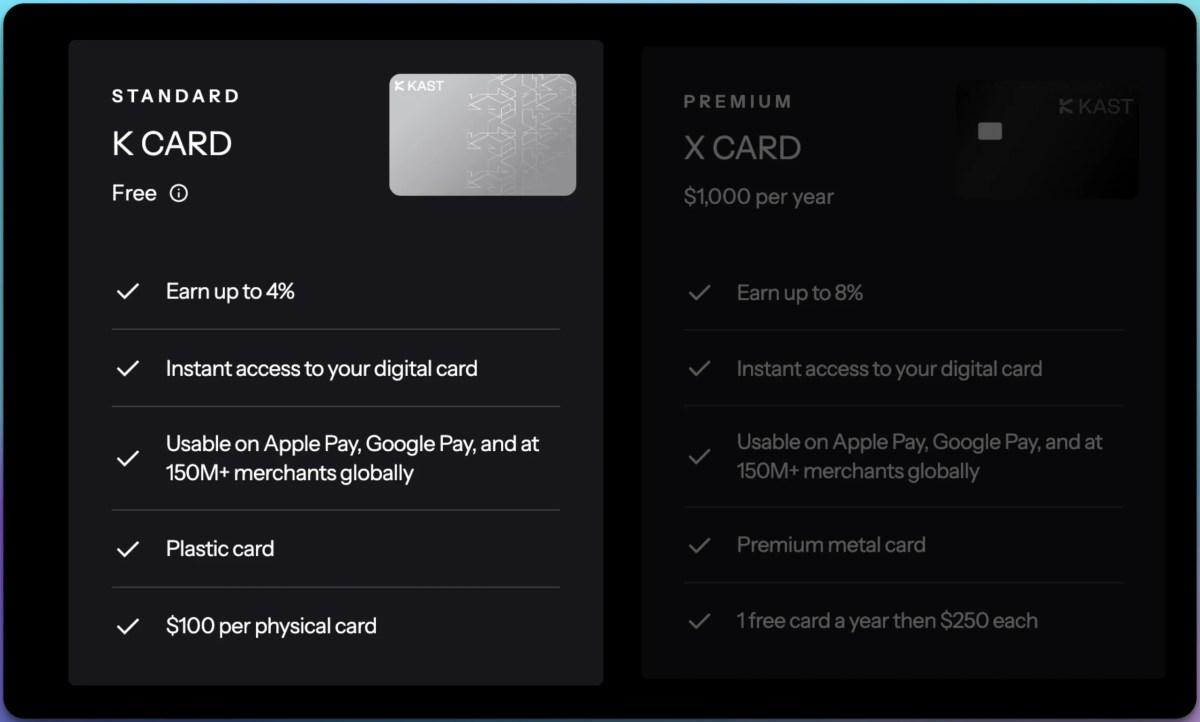

Ownership Costs and Maintenance Surprises

A low monthly fee or a free initial card is just the entry price. The real cost of owning a prepaid card like the STABLE Card often hides in the details that only appear after you’ve been using it for a while. What looks cheap on day one can become expensive if you don’t understand the fee structure.

The Hidden Costs of Inactivity

Many prepaid cards charge monthly maintenance fees if you don’t use them regularly. These fees can eat away at your balance even if you’re not spending. Some providers waive these fees if you make a certain number of transactions or load money monthly, but the rules vary. If you plan to keep the card for emergencies only, check if the monthly fee applies regardless of usage.

Reload and Transfer Fees

Adding money to your card isn’t always free. While some methods like direct deposit or bank transfers might be free, other options like retail reloads, wire transfers, or third-party apps can carry fees. For example, STABLE allows you to load up to $20,000, but the method you choose matters. If you frequently need to top up quickly, look for cards that offer free instant reloads via linked bank accounts or debit cards.

ATM and Foreign Transaction Fees

If you need cash or travel, ATM withdrawal fees and foreign transaction fees can add up. Some cards charge a flat fee per ATM withdrawal, plus any fee the ATM operator charges. Foreign transaction fees are often a percentage of the purchase amount. If you don’t travel or use ATMs often, this might not be a big concern, but it’s worth checking if you plan to use your card internationally.

When a Cheap Card Stops Being Cheap

A card with a $5 monthly fee might seem affordable, but if you’re only using it for occasional purchases, that fee adds up to $60 a year. Compare this to a card with no monthly fee but higher transaction fees. If you make many small purchases, the no-fee card might end up costing more. Calculate your expected usage—how often you’ll reload, withdraw cash, or make purchases—to find the most cost-effective option.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!