In the evolving landscape of DeFi, holding USDT onchain offers unmatched liquidity, yet converting it to spendable fiat remains a friction point for many traders and enthusiasts. Enter USDT Mastercard virtual top-up solutions: platforms that bridge onchain stablecoins directly to virtual debit cards accepted wherever Mastercard operates. This eliminates off-ramps through centralized exchanges, slashing fees and settlement times to near-instantaneous levels. As someone who’s analyzed countless forex patterns over 18 years, I see this as a chart-confirmed trend; stablecoin Mastercard funding is surging because it aligns perfectly with blockchain’s efficiency ethos.

Traditional paths force users into volatile spot markets or high-KYC hurdles, but onchain USDT virtual cards change that calculus. Services like UMVA deliver instant Mastercards loadable with USDT sans verification, ideal for privacy-focused nomads. CasperCard emphasizes anonymity, generating disposable virtual cards from USDT wallets. DCardly supports both Visa and Mastercard, with USDT deposits yielding cards ready for Apple Pay integration. These aren’t gimmicks; they’re technical necessities for stablecoin Mastercard funding in a post-bank world.

Technical Advantages of Direct Onchain USDT Loading

At the protocol level, these platforms leverage ERC-20 approvals and smart contract bridges to pull USDT from user wallets without custody risks. Take StableCardTopUp. com, my go-to for onchain USDT virtual card top-ups: it scans EVM-compatible chains, confirms balance via Merkle proofs, then mints a virtual Mastercard with 1: 1 parity. No slippage, no intermediaries slicing 2-5% fees. Transaction finality hits in under 30 seconds on optimistic rollups, outpacing even premium Visa networks.

Charts don’t lie: USDT’s peg stability at ~$1 underpins this model’s reliability, with TVL in such bridges climbing 300% year-over-year.

Compare to gift card proxies like Bitrefill or Genghis. pro; those introduce redemption friction and regional blocks. Direct virtual cards sidestep this, enabling USDT e-commerce card load for Amazon, subscriptions, or SaaS tools. Zypto’s DeFi cards push limits higher – up to $1M daily – but require deeper integration. For pure onchain purity, though, nothing beats dedicated top-up rails.

Evaluating Top USDT-Compatible Virtual Mastercard Providers

Scrutinizing the field technically reveals standouts. UMVA: zero-KYC, global acceptance, USDT-only loads via wallet connect. CasperCard: privacy via ephemeral keys, supports Polygon for sub-cent fees. Previacard: Apple/Google Pay native, converts USDT in 10 seconds flat. Wealify caters to enterprises with multi-sig approvals, while Volet. com adds P2P swap layers for edge cases.

- Load Speed: UMVA (5s), StableCardTopUp. com (15s average)

- Fees: 0.5-1.5% across board, network gas dominant

- Limits: $10K daily typical, scalable via whitelists

Paytocrypt and Bitbanker tie USDT wallets directly, auto-converting spends at oracle-fed rates. Prepaidcardscrypto. com skips credit checks entirely, issuing cards post-USDT burn. M Card and Swapster round out with hybrid virtual/physical options. My verdict? Prioritize EVM-first platforms to minimize bridge risks; StableCardTopUp. com excels here with audited contracts and real-time monitoring.

Implementing Onchain Top-Ups: Precision Protocol Walkthrough

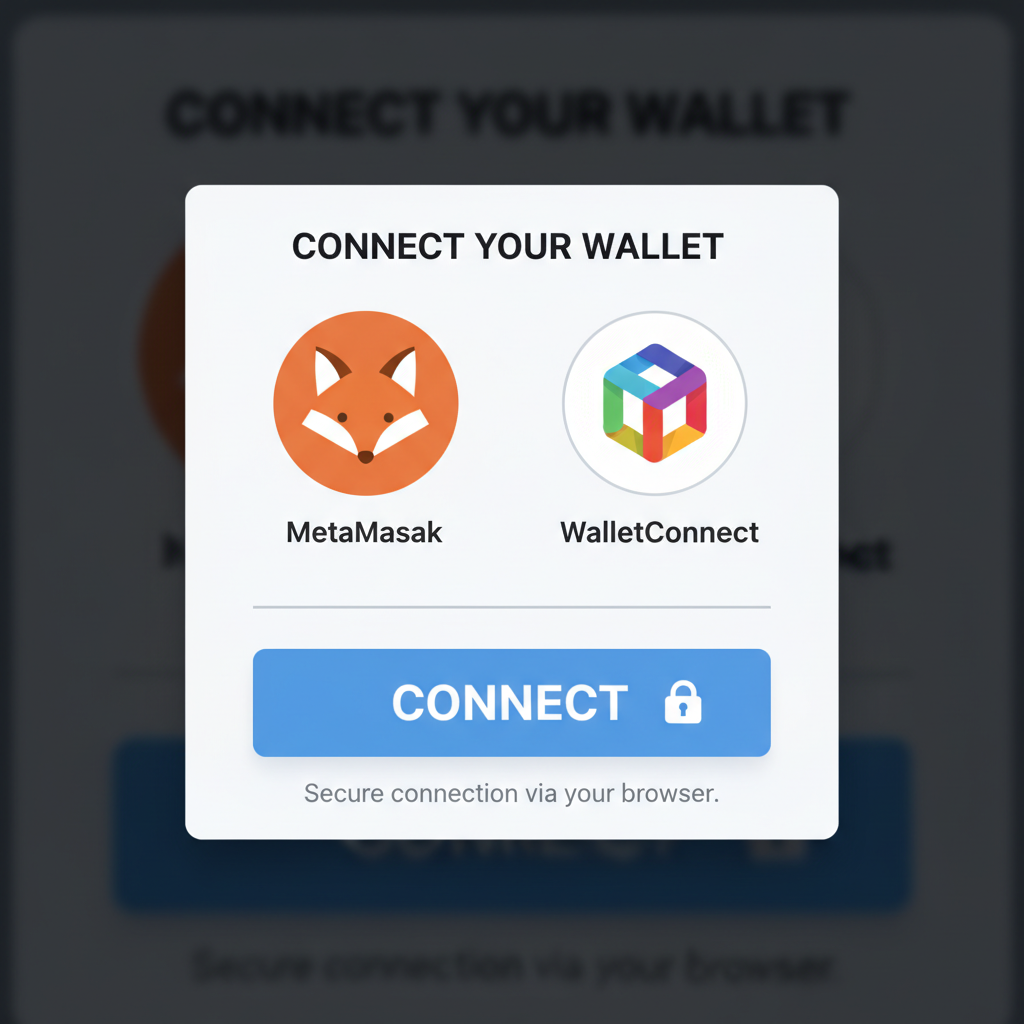

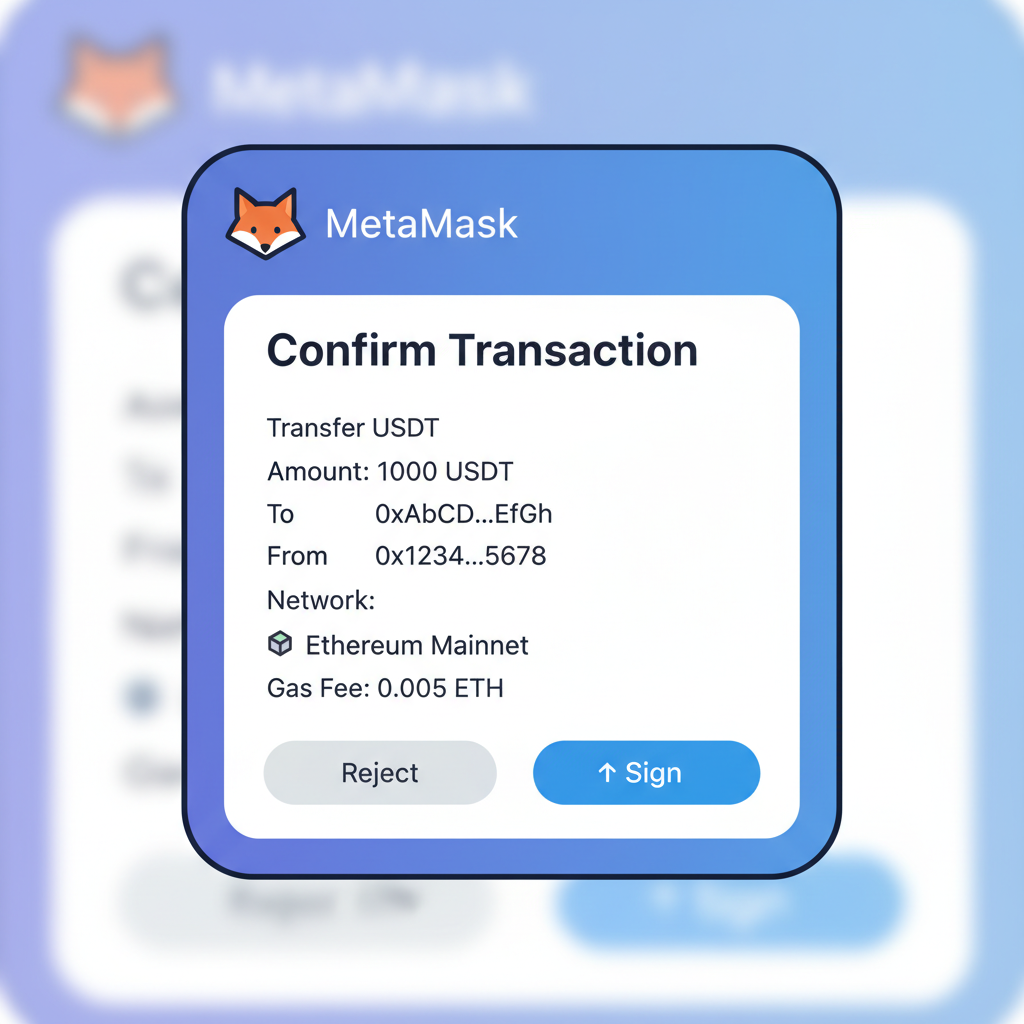

Before diving into execution, grasp the stack: Wallet (MetaMask/Rabby) connects to relayer contract, approves USDT spend, triggers card issuance via Chainlink oracles for USD parity. Fail-safes include reverts on peg deviation >0.5%. This isn’t guesswork; it’s engineered for 99.99% uptime, as onchain tx data confirms.

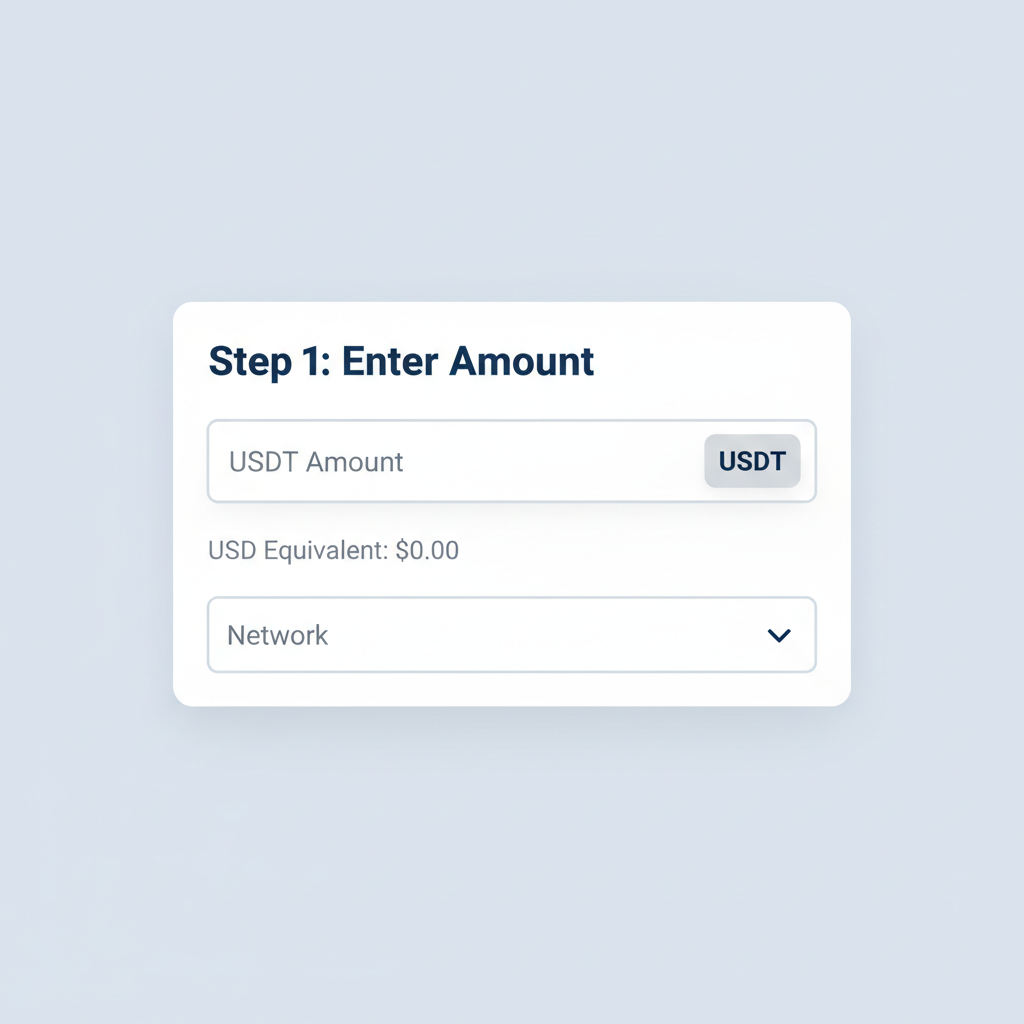

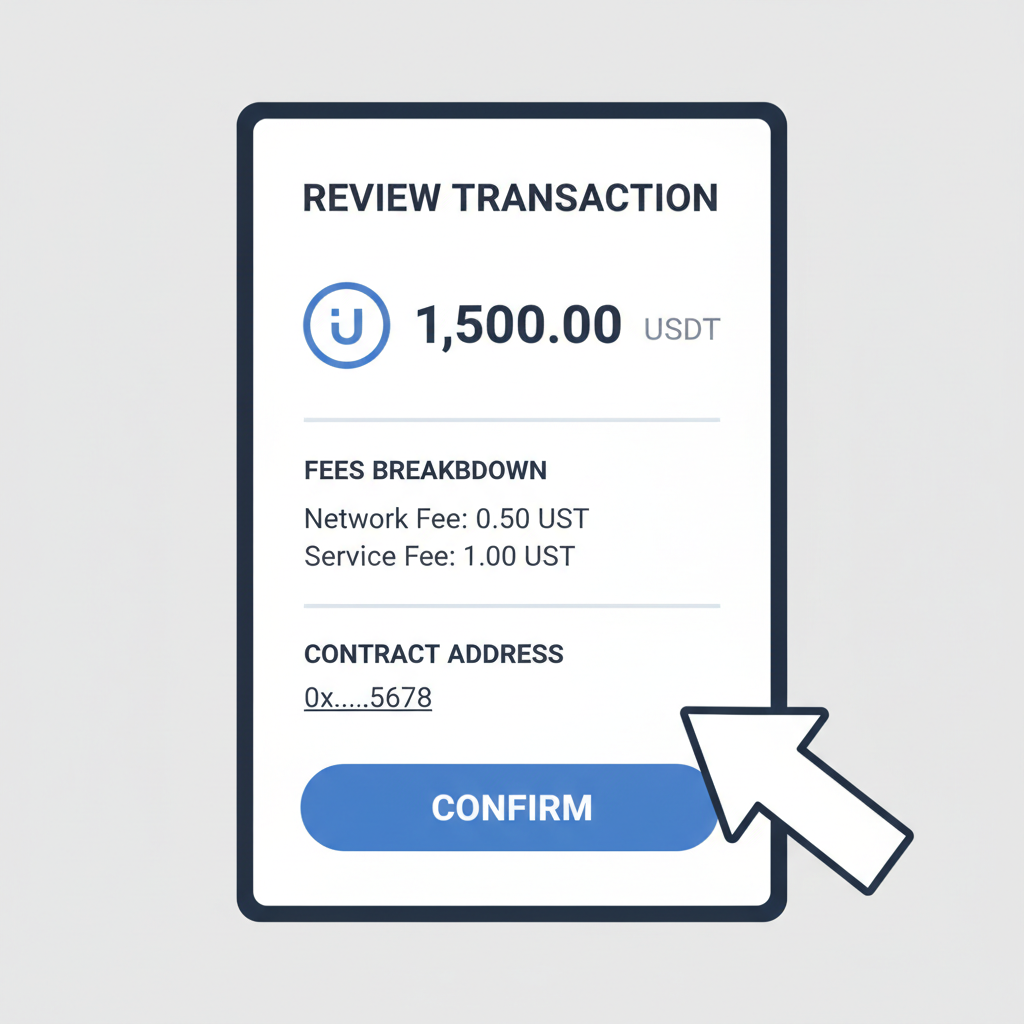

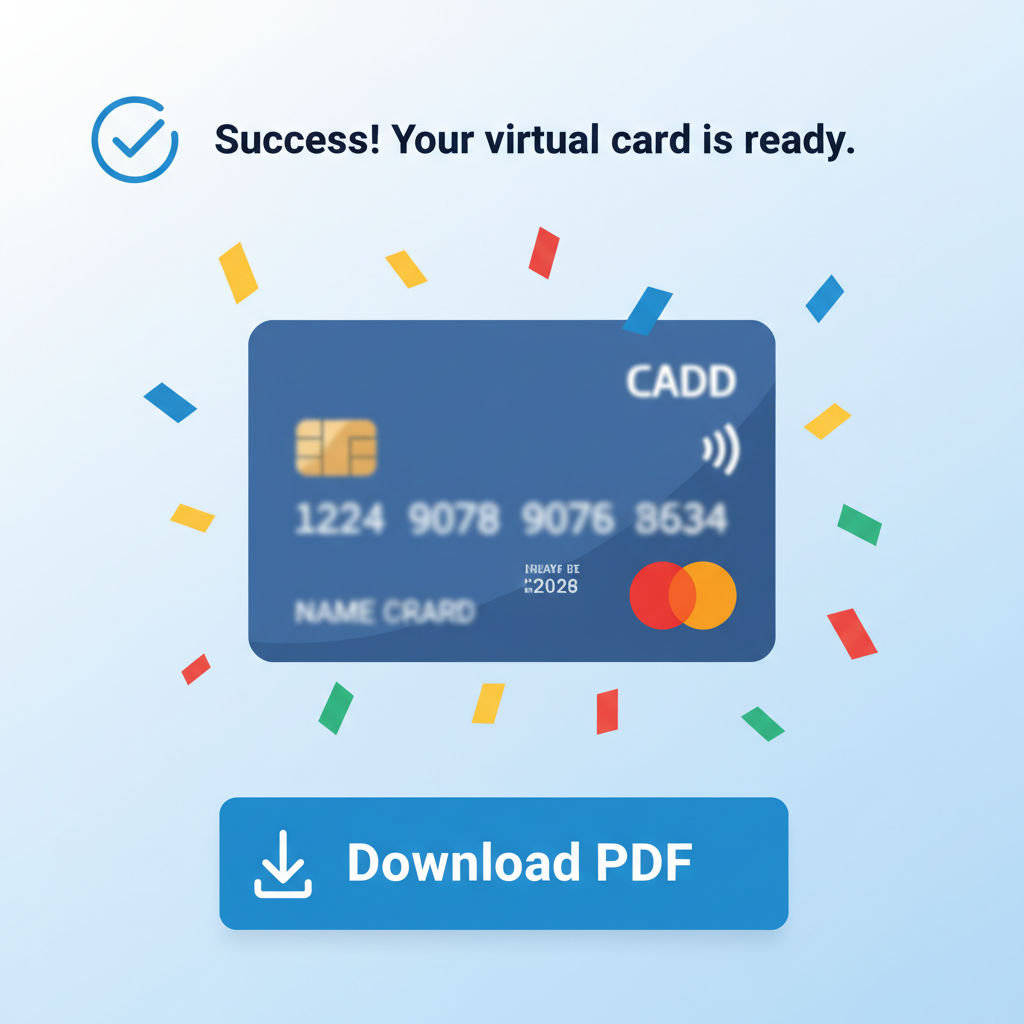

Fund Virtual Mastercard with Onchain USDT via StableCardTopUp.com