In the evolving landscape of blockchain finance, onchain stablecoin funding for everyday virtual debit spending represents a pivotal shift. Platforms like StableCardTopUp. com enable users to top up virtual and physical debit cards directly from USDC, USDT, or DAI balances, sidestepping banks and exchanges. This approach delivers low-fee, secure conversions, turning onchain liquidity into immediate purchasing power for DeFi users and traders alike.

The demand for such solutions surges as stablecoins mature beyond trading instruments into practical spending tools. Recent developments, including Phantom Wallet's debit card rollout and Visa's partnership with Baanx, underscore this trend. Users now spend USDC directly from self-custodial wallets via smart contracts, with conversions handled at point-of-sale for seamless Visa and Mastercard acceptance.

Key Platforms Driving Onchain Adoption

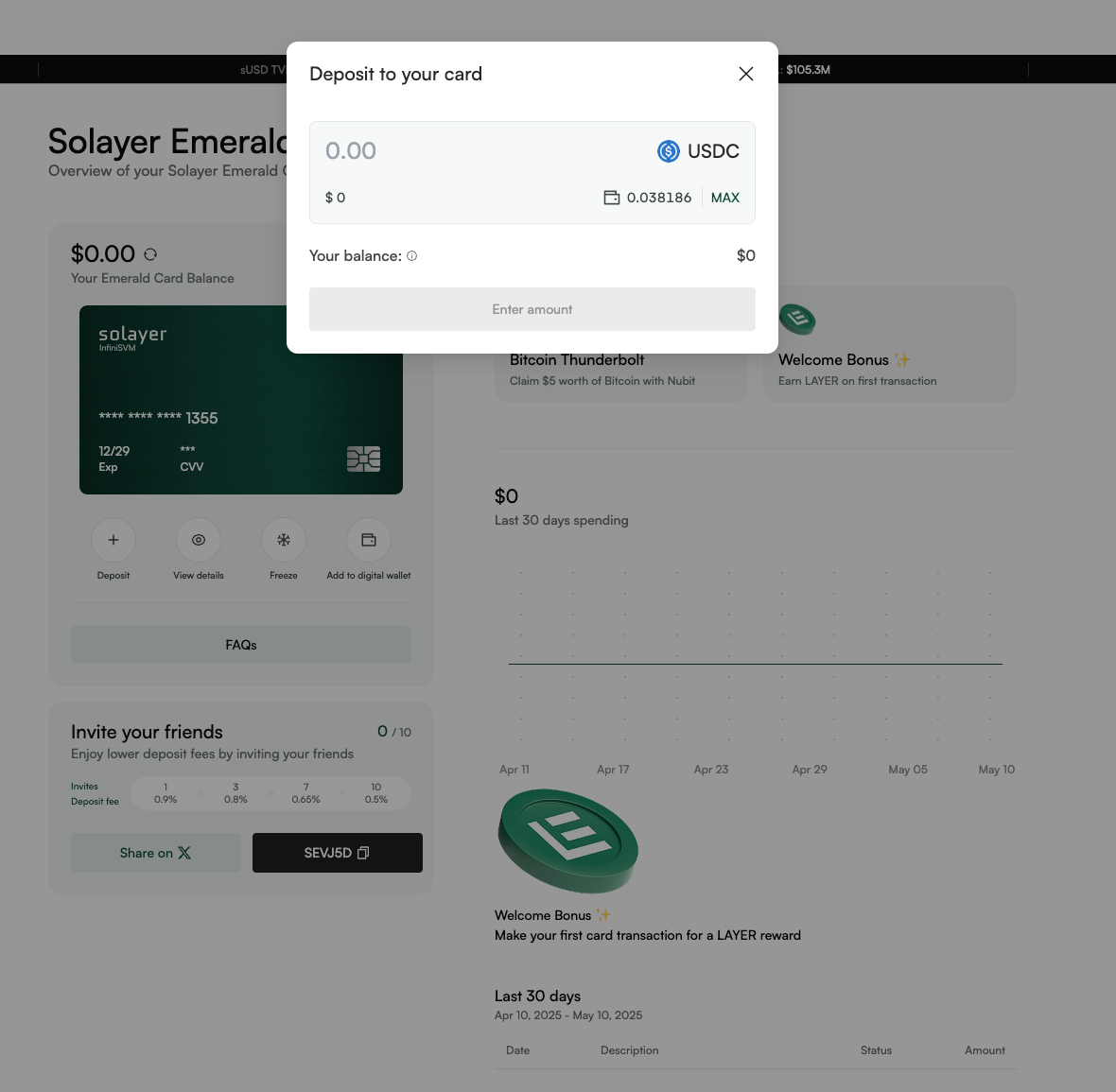

Holyheld stands out with its non-custodial virtual debit card, allowing crypto natives to pay from their phones using preferred stablecoins. Issuance is instant, and every purchase earns up to 1% cashback in USDC. Phantom Cash, backed by Solana's dollar-pegged CASH stablecoin, integrates with Apple Pay and Google Pay, mimicking traditional debit experiences while keeping funds onchain until needed.

Essential Features of Top Onchain Stablecoin Cards

- Instant Issuance: Holyheld provides virtual cards usable immediately upon issuance for quick setup.

- Non-Custodial Funding: Holyheld and Baanx enable spending directly from self-custodial wallets using onchain mechanisms like smart contracts.

- Cashback Rewards: Holyheld offers 1% cashback in USDC on purchases; Bitget Wallet Card provides up to 18% APY plus spending rewards.

- Apple/Google Pay Support: Phantom Wallet debit card integrates with Apple Pay and Google Pay for contactless payments.

- Global Visa/Mastercard Compatibility: Cards such as Baanx Visa and Immersve Mastercard are accepted worldwide on these networks.

RedotPay complements this space by offering virtual and physical cards for stablecoin spending online and in-store. Bitget Wallet Card adds value through up to 18% APY on stablecoin earns plus rewards, while KAST provides seasonal cashback up to 12%. These options address the missing link Gate. com highlights: transforming USDT from onchain assets into everyday tools.

Mechanics of Stablecoin-to-Debit Top-Ups

At core, these systems rely on smart contracts for authorization. When a card is used, the platform pulls from the user's onchain balance, converts to fiat instantaneously, and settles with merchants. Circle's collaboration with Immersve exemplifies this, enabling USDC spending anywhere Mastercard works. Baanx's Visa cards extend similar functionality, prioritizing self-custody to minimize counterparty risk.

CoinGecko notes high limits - daily up to $12,000, annual around $150,000 - suit regular and travel spending. Stripe emphasizes benefits like speed and low costs, though risks such as volatility exposure during conversion warrant caution. Conservative users appreciate the control: no pre-funding custodial accounts, just direct onchain pulls.

Risks and Rewards in Daily Integration

While rewards like cashback and yields entice, analytical scrutiny reveals nuances. Platforms optimize for stablecoin virtual debit everyday use, but gas fees on Ethereum can erode margins versus Solana alternatives. Reddit discussions praise instant virtual cards for shopping, funded in seconds across major networks. Yet, regulatory shifts demand vigilance; U. S. rollouts like Phantom's signal maturing infrastructure.

StableCardTopUp. com optimizes this with blockchain efficiency, supporting USDT USDC DAI card top up for global networks. For everyday spenders, debit card onchain balance management offers liquidity without limits, provided users select low-volatility chains and monitor conversion spreads.

Practical implementation requires a measured approach, balancing efficiency with prudence. DeFi enthusiasts often overlook chain selection, yet Ethereum's congestion contrasts sharply with Solana's throughput, directly impacting onchain funding daily spending costs. Platforms like Holyheld mitigate this by supporting multiple chains, ensuring users retain sovereignty over their assets.

Optimizing Everyday Use Cases

Virtual debit cards shine for online subscriptions, travel bookings, and impulse buys, where immediacy trumps permanence. Physical variants, as in RedotPay's offerings, extend utility to point-of-sale transactions, bridging the gap Stripe identifies between stablecoins' stability and fiat's ubiquity. Bitget's high APYs tempt yield farmers, but conservative portfolios prioritize cashback consistency over speculative returns. KAST's seasonal boosts exemplify targeted incentives, rewarding measured spending patterns rather than profligacy.

Fund Your Virtual Debit Card with USDC, USDT, or DAI on StableCardTopUp.com

Gate. com aptly terms USDT cards the missing link, yet true innovation lies in non-custodial execution. Baanx's Visa integration with Circle's USDC deploys smart contracts for just-in-time conversions, minimizing idle fiat exposure. Phantom's Solana-backed CASH card further democratizes access, folding seamlessly into Apple Pay ecosystems without app proliferation. CoinGecko's limit benchmarks - $12,000 daily, $150,000 annually - accommodate most lifestyles, from urban commuters to globetrotters.

Reddit threads reveal real-world traction: users fund virtual cards in seconds for Amazon hauls or Netflix renewals, evading exchange KYC hurdles. Binance's Lightning analogy applies loosely; stablecoins sidestep Bitcoin's volatility, focusing on pegged precision for stablecoin virtual debit everyday routines.

Strategic Considerations for Long-Term Viability

Regulatory headwinds loom, particularly in the U. S. , where Phantom's rollout tests FinCEN compliance. Conservative investors hedge by diversifying across providers: pair Holyheld's instant issuance with StableCardTopUp. com's broad stablecoin support. Monitor spreads vigilantly; a 0.5% conversion premium compounds on frequent use, eroding the low-fee promise. Yet, yields and rebates often offset this, netting positive economics for disciplined spenders.

| Platform | Key Feature | Rewards |

|---|---|---|

| Holyheld | Non-custodial wallet integration | 1% USDC cashback |

| Phantom Cash | Apple/Google Pay support | Seamless POS conversion |

| Bitget Wallet | High spending limits | Up to 18% APY |

Immersve's Mastercard pathway via Circle underscores enterprise traction, hinting at broader adoption. For the everyday user, StableCardTopUp. com distills these advancements into a streamlined portal, facilitating USDT USDC DAI card top up without navigational friction. Select virtual for ephemerality, physical for tangibility; either way, onchain balances fuel unencumbered commerce.

This ecosystem matures unevenly, favoring chains with robust DeFi liquidity. Solana's edge in speed suits high-velocity spending, while Ethereum's security appeals to purists. Ultimately, debit card onchain balance strategies empower users to navigate fiat realms on their terms, preserving the autonomy blockchain promised. Platforms evolving in lockstep with user needs will define the next era of spending sovereignty.

No comments yet. Be the first to share your thoughts!